The Real Cost of Staying Still in Today’s Property Market

Many homeowners think “staying still is safe.” But in today’s and future markets, staying still without understanding can quietly reduce your options — especially when retirement comes into the picture.

Staying Still Feels Safe — But What Is the Hidden Cost?

Many homeowners believe that staying still is the safest move.

After a strong run-up in recent years, it’s natural for homeowners to feel cautious. No risk. No regret. No pressure.

But in today’s and future property markets, staying still without understanding the implications can quietly become a risk of its own.

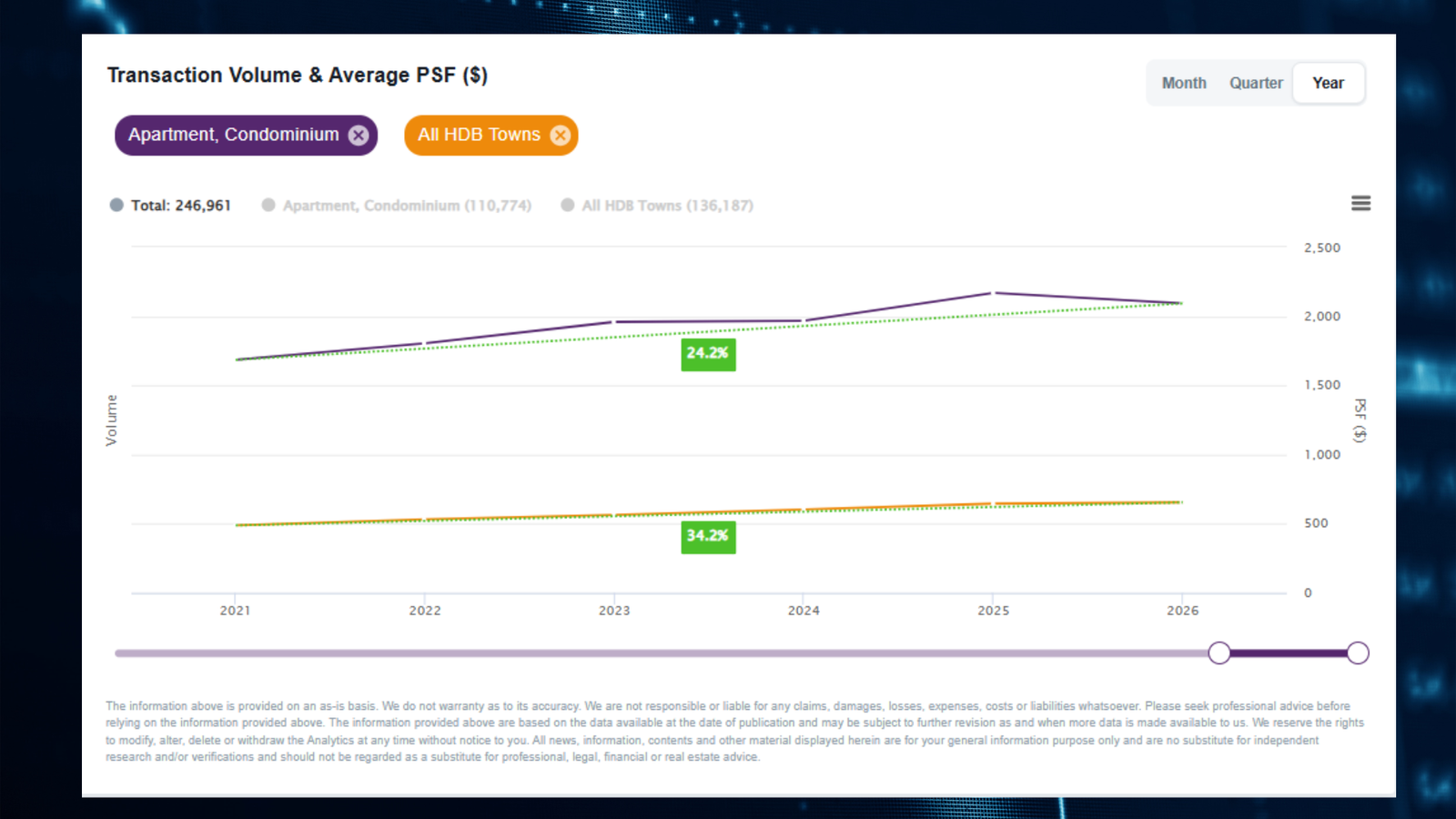

Losing Relative Ground (Even If Prices Go Up)

One of the most misunderstood risks is relative loss.

Your HDB flat may continue to appreciate modestly over time. But if private property continues its gradual, compounding growth while HDB growth normalises, the upgrade gap can widen again.

You didn’t lose money — but you may lose the ability to move up later without significantly more effort, cash, or risk.

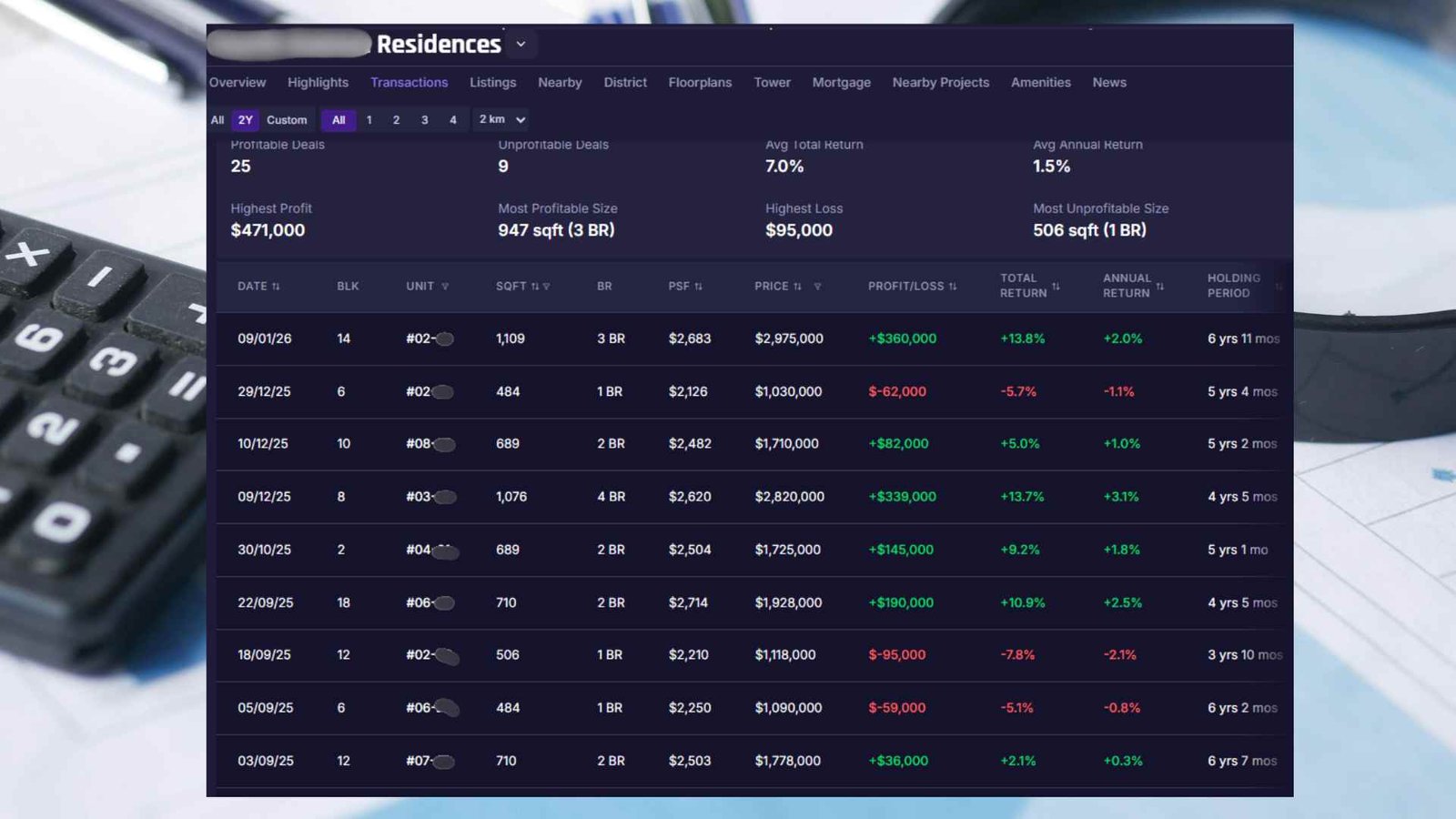

Exit Risk Increases With Time

Every property has an exit profile.

For HDB owners, staying longer means a shorter remaining lease, a more price-sensitive buyer pool, and greater dependence on policy and affordability limits.

Strong exits don’t happen by chance. They are usually the result of timing and planning, not waiting indefinitely.

Retirement Reality Is Often Overlooked

Property is not just a home — for many Singaporeans, it is also a retirement asset.

As time passes, retirement periods grow longer (20–25 years is increasingly common), and inflation continues to erode purchasing power.

Why this matters

- Inflation reduces what your money can buy over time.

- Replacement costs (land + construction) tend to trend upward long-term.

- Your home may go up — but the next home you want may go up faster.

Not All Properties Are Equal (Good vs Bad Choices)

Some homeowners fear upgrading because they worry about buying at the wrong time, choosing the wrong property, or making a mistake. That fear is valid — not all properties are good assets.

Some private properties preserve and grow value. Others stagnate, become difficult to exit, and add stress instead of security.

Jumping in blindly can be costly — but there is another hidden risk: not understanding the difference early enough. Many people don’t regret buying property. They regret buying the wrong one — or waiting too long to learn what makes a good one.

Optionality Shrinks Over Time

Time gives you options.

When you plan early, you can compare projects, choose layouts and locations, and avoid rushed decisions. When you wait too long, choices narrow, decisions become reactive, and mistakes become expensive.

Optionality has value — and it fades quietly.

So… Is Staying Still Wrong?

No.

Staying still can be a perfectly valid decision if it is informed and intentional.

But staying still by default, without understanding your future exit, retirement implications, and the difference between good and bad next-step options… is where risk begins to build.

The Right Question to Ask

It’s: “If I do nothing, what does that cost me over the next 5–10 years?”

Because in property, inaction is still a decision — and retirement makes that decision permanent.

Want clarity without pressure?

If you’re unsure whether staying put, upgrading, or restructuring your property makes sense for your long-term plans, start with understanding — not guessing.

Get a clear plan for your next move